And that is it until the House sits on Tuesday – if that works for you?

Thank you so much for joining us as we waded through what we all knew was about to happen – it can always be a drag following along with the predictable.

Next week the house sits, and it is also senate estimates – which we will bring you, so hopefully we will see you there?

As always, you can catch me on the socials, or on email – but until then, take care of you. Ax

16.06 AEST

And the press conference ends – that is the RBA done for another meeting.

15.57 AEST

The View from Matt Grudnoff

Matt Grudnoff

Senior Economist

Michele Bullock points out that many people are not spending the three interest rate cuts but instead are using them to pay off their mortgages faster. Lower interest rates only stimulate the economy if the money is spent.

This is likely because people have been scarred by the big increases in prices and higher mortgage rates. Many were caught out and faced real financial pain. Now that real wages are growing again and they are not facing as much financial pain, they don’t want to loosen their belts and spend. Why? Because they want to build up a buffer in case something like this happens again.

15.51 AEST

And a bit more

Greg Jericho

Chief Economist

Bullock gives an interesting (if a bit nerdy) note on the new monthly CPI that will begin in November:

“From November we are getting a full monthly CPI rather than a partial indicator which we’ve got at the moment. And I want to say that’s great news every nearly every other country in the world has a monthly CPI I think, or advanced economies. So this will bring us in line with that. So that’ll be great.”

But!!!

A couple of points though when it comes in the monthly CPI will be more volatile than the quarterly. It just will because it’ll be monthly data rather than quarterly data. Second point is that the monthly Outtrim mean is not calculated in the same way the quarterly trimmed mean is. Our focus is the quarterly trimmed mean. We think that’s the best measure of underlying inflation. So our focus will not be on the monthly trimmed mean we’re not going to be focusing on that.”

So don’t expect much change in how the RBA goes about making decisions even when we get more regular inflation figures.

15.46 AEST

The view from Grogs

Greg Jericho

Chief Economist

Michele Bullock begins her press conference by basically reading out the board statement.

Then the questions start.

She tells Reuters that she “think the economy still is in a good spot”.

And then to a journalist form Newswire who oddly seems to be concerned that prices are not going to go down that “the fact is that prices have risen and their staying up there permanently. We’re not going to see a decline in we don’t want to see deflation. Deflation is not good for businesses.” This is quite correct – prices falling across the board is Great Depression time. The key is to ensure wages are able to rise in such a way as to recover the lost living standards.

Unlike in the previous meeting, today Bullock is not giving any forward guidance on whether rates will likely go down or stay steady (which really means they will stay steady)

Bullock then says that she thinks the current interest rate is “probably a little bit restrictive” – ie she thinks the current cash rate is slowing the economy (causing unemployment to rise). She then adds “So how restrictive are we at the moment? I don’t know. So we’re really that’s why we have to be data dependent. We have to see what the outcomes are looking like, what the forward looking indicators are telling us and what our forecasts are telling us.” And I guess it is good to hear the Governor of the Reserve Bank admit that she doesn’t know how much the setting of interest rates is slowing the economy, but also a bit concerning. It does however highlight that those going around thinking economic policy is a precise activity are very much wrong.

15.44 AEST

Can borrowers expect rates to go down before the end of the year still?

So, can we expect the RBA to look at decreasing rates before the end of the year? Michele Bullock says “it depends”.

It’s all depended on the particular meeting. And I think what you’re referring to was the July meeting when we didn’t move. And I think at that meeting what I said was people were thinking the next move was probably down, but it was a question of timing. So they were sort of meeting specific comments, I think in that particular context, in terms of what people should expect now, I’m not going to give forward guidance.

I think I’ve said that a number of times, but what I would say is that today we felt given the evidence we had the were reasonably balanced, that there had been a bit of an upside surprise on some of the data, the inflation and the activity data. And I should say that’s good news. It’s good news that activity is responding.

So I don’t want anyone to think that’s bad news, but it just makes us think, well we’ve got another. It was a good decision today to hold. We’ll have more information available in November and we’re looking forward. We’re trying to see where this might take us in terms of inflation and employment. And then we can make a decision in November.

So we’ll make that decision in November about whether it’s down again or maybe it’s hold again. And if the economy is continuing to recover that’s really good news.

15.40 AEST

Don’t expect prices to return to pre-covid levels

The RBA Governor is also reiterating that consumers can not expect to see prices fall, just because inflation has.

Bullock:

The fact is that prices have risen and their staying up there permanently. We’re not going to see a decline in we don’t want to see deflation. Deflation is not good for businesses. It’s not good for making investment decisions. That’s why low and stable inflation is best when it’s in the background and it isn’t influencing decisions. But I’m just want people to understand that when we’re lowering inflation, that doesn’t mean we are lowering the price level. We’re lowering the rate at which prices are increasing.

15.36 AEST

RBA Governor: ‘Economy is in a good spot’

Michele Bullock is feeling OK about the overall economy though (no one tell Ted O’Brien)

I mean, we have inflation basically in the 2 to 3% range. The unemployment rate is holding at around 4.2. We expect it will drift up a little bit, but we still expect it to be relatively low compared with history. The monthly data are volatile, but a couple of components. We’ve got two months now of the quarterly number and a couple of components. A market services and housing inflation were a little more a little higher than we’re expecting. So we’re just being a little bit cautious about that. It doesn’t I don’t think suggest that inflation is running away. But we just need to be a little bit cautious.

15.35 AEST

RBA Governor: ‘Monetary policy working as expected’

Michele Bullock is holding her press conference and says that monetary policy is doing its job, but the RBA is worried about some of the lag of the earlier rate rises (it takes time for the impacts of rate cuts to flow through to the economy)

Here is her opening statement:

On balance, domestic data since the August meeting have been in line with or a little stronger than what we’re expecting in our forecasts. The labour market remains solid, and although employment growth has been slower in recent months, we judge it’s still a little tight relative to full employment. Inflation remains within the target range, but recent data indicate there could be a bit more upward pressure than we thought, in August.

The June quarter national accounts also gave us a bit more confidence that recovery in the private sector demand, particularly household consumption, is progressing as we expect in our August forecasts, we expected global growth to slow, partly reflecting the impact of tariffs and changing trade flows.

Since then, there has been some weaker than expected data from China, but the trade volumes have held up and it’s still expected that the authorities would provide support if needed. Data from the United States has been more mixed with weak employment data, but relatively strong activity data.

The board sees the risks as broadly balanced and it remains data driven by the next meeting in November, we’ll have more data on the labour market and inflation data for the September quarter. We’ll also have some more forward looking indicators, including from liaison and an updated set of forecasts.

We know that high inflation has pushed up prices across the board over the past few years. And while inflation has fallen a lot, the price level isn’t coming back down and this higher price level affects everyone. And it’s been especially tough on people of lower incomes and the more vulnerable. This is why it’s so important to keep inflation low and stable and unemployment as low as possible.

15.26 AEST

Grogs is going to watch Michele Bullock at the RBA press conference, so you don’t have to.

Thank you, Grogs.

15.12 AEST

The current shadow treasurer is holding a press conference

You do not have to read this – it matters as much as yelling at the clouds.

But for those who have a burning desire to hear from the current shadow treasurer (who is indistinguishable from a beige wall on the best of days) here is what Super Ted O’Brien has to say:

Right across the country, the average mortgage holder will be paying $1,800 more in interest payments every single month compared to when the Coalition was in government. That will continue to be the case. My heart goes out to not only to them today, but my heart also goes out to all of those young Australians who are hoping to get into the property market. The higher these interest rates are, the tougher it’s going to be for younger Australians who want to chase that Australian dream of owning their own home. What we hear from the Reserve Bank is if you look at their just the first paragraph in their statement today that inflation in the September quarter was higher than expected.

This is a direct consequence of the Albanese government’s spending spree. There is a reason why rates have been higher for longer in Australia, and that is this Albanese government ensuring that they keep spending and a big government approach is their mode of operation. This has not changed and we continue to see that in the figures that are released over time. This government is spending $160 billion extra, $160 billion extra this financial year compared to when the Coalition was in government. This is leading to a larger non-market sector crowding out the private sector. We’re seeing productivity go backwards. Productivity has gone backwards by over 5% under this government’s watch, which is why we have seen Australia experience the deepest falls in living standards across the developed world. If you look at the OECD, our productivity is the second worst. Now what this means is not only on one hand is the government on a spending spree, but on the other hand it is failing to grow the Australian economy. And this leaves very little room for the Reserve Bank when it comes to monetary policy.

15.05 AEST

Crystal ball time

Is Jim Chalmers worried that the RBA won’t cut interest rates before the end of the year?

Chalmers:

I don’t engage in that kind of commentary. We’ve seen interest rates cut three times already this year when we came to office. Interest rates were already rising. Inflation was around double what it is now and rising fast. We’ve been able to get inflation down. We’ve seen interest rates cut multiple times. As a consequence we’ve got real wages growing.

We’ve kept unemployment low. We’ve got the budget in better Nick. So all of that represents good progress. But we know that there is more work to do. People are still under pressure. They’re getting some welcome relief from those three rate cuts. Earlier this year.

They’re getting relief from the government in the form of tax cuts and responsible cost of living help. But we know that there’s almost always more work to

14.59 AEST

Jim Chalmers press conference

The treasurer is very well prepared for this press conference – it is exactly as he expected.

Chalmers:

This is not the outcome that millions of Australian home owners would have wanted but it’s certainly the outcome that markets and economists were expecting. Interest rates have already come down three times in six months this year and that’s a very good thing. The three interest rate cuts which are already in the system are already providing very welcome relief to millions of Australians with a mortgage.

For a household with a mortgage of $700,000, the rate cuts this year means they are saving about $330 a month – or about $4,000 a year. Now, the progress that we have made together on inflation this year has already given the Reserve Bank the confidence to cut interest rates three times in that 6-month period.

Now, we know that when interest rates are cut around the world, they’re not always cut at every meeting or indeed every couple of meetings and so this outcome today from the independent Reserve Bank is not a surprise to the government.

14.50 AEST

Response from the Treasurer

Jim Chalmers has released a statement:

Today the independent Reserve Bank of Australia Monetary Policy Board kept interest rates on hold at 3.60 per cent.

While millions of Australians would’ve wanted to see more rate relief, this decision was widely anticipated and widely expected by markets and economists.

Rates have already come down three times this year and that’s a good thing.

That’s because we’ve made very substantial and sustained progress together on inflation over the past three years.

For a household with a mortgage of $700,000, the three rate cuts mean they are saving about $330 a month, or about $4,000 per year.

On the most reliable measure, headline and underlying inflation have both fallen to their lowest rates in almost four years, and are back in the Reserve Bank’s target band.

We’ve seen around the world that as central banks cut rates, they don’t always cut them at every meeting.

When we came to office, headline inflation was 6.1 per cent and rising, it’s now much less than half of that.

When we came to office, trimmed mean inflation was 4.9 per cent and rising, it’s now almost half of that.

This progress comes at the same time as we’ve seen inflation tick up in parts of the world including the United States, Canada and New Zealand and remain stubbornly high in places like the United Kingdom.

The RBA’s statement makes it clear that economic uncertainty is “elevated” around the world which could weigh on global growth.

In the face of this substantial global economic uncertainty and volatility, Australians have made remarkable progress together in the economy.

We’ve managed to get inflation down while keeping unemployment low, growing the economy and getting the budget in better nick as we saw in the 2024-25 Final Budget Outcome earlier this week.

We saw a welcome and substantial pick-up in economic growth in the most recent data, and as the RBA’s statement highlights the private sector has resumed its place as the primary driver of growth in our economy.

While we have made good progress on the economy, we understand that people remain under pressure.

That’s why the Government is rolling out responsible cost of living relief including two further rounds of tax cuts, energy bill relief for every household, cheaper medicines and cutting student debt.

Under Labor, inflation is down, unemployment is low, real wages and living standards are growing again, more than 1.1 million jobs have been created, debt is down, the economy is growing and interest rates have fallen.

We know the job is not finished because people are still under pressure and there’s more to do to make our economy more productive and dynamic.

14.47 AEST

And on another note

Greg Jericho

Chief Economist

Readers will likely have heard that today Donald Trump has once again mooted putting a 100% tariff on foreign films.

In a former life I was involved in the administration of the Location Tax Offset in the Department of Communications and the Arts, so I know a (very) little bit about film budgets and production. And to say they are complicated is an understatement of the order of saying Donald Trump seems a bit iffy on issues of race.

The problem of course is that if this tariff did come into effect (and Trump has often thrown out a few thought bubbles that have come to nought so let’s not assume anything) it would destroy Australia’s film sector.

Our film sector relies of tax offsets that give a 30% tax rebate on any expenditure done on the film in Australia. This is why we had films like The Fall Guy made here – it was good value for the film company to make it here. (especially given US$1 = around A$1.50). It is also good for the local film production crew because they get to work on a big budget film that means they can invest in better equipment, employ more people than they could were they only reliant on local film. It also means (theoretically at least) that when working on local films they also can make use of the new equipment, so we end up with better Australian films.

A 100% tariff would make producing US films in Australia unviable, and given it would also make selling Australian films to the US double the cost, it would reduce a great deal of the incentive for making local films, if you effectively had no chance of selling it to the biggest film market.

But – and it is a big BUT – how would the tariff be levied?

When you import a good – like a car – you pay a tariff as it comes through customs. That’s not how film production works. Let’s say a US film company makes a film in Sydney – what is the thing that is having a tariff on it? Do you charge a tariff on the cost of making the film? What if only part of the film is made in Australia? What if only the PDV (special effects) is done here (we have a number of world leading PDV companies)? What is the tariff then?

Putting a tariff on services is tough because services are paid outside of the US – so there is no point for the US govt to hold up an import until a tariff is paid. It could be easier for film in theatres – you could potentially find a way to slap a tax on cinema tickets for certain films, but what about streaming where there is no cost on an individual film or TV show?

Putting a tariff on Australian made films would be somewhat easier – but that would do precisely zero for the US film industry. The big thing Trump wants to prevent is US films being made overseas – and that is a much tougher thing to put a tariff on.

So let us wait and see where this goes. My gut says it is more of a threat for companies like Disney etc to do what Trump wants with people like Jimmy Kimmel than anything else.

14.46 AEST

The view from Grogs

The RBA has kept rates at 3.6% mostly because they think their forecast done back… August… are wrong.

The policy statement noted “Recent data, while partial and volatile, suggest that inflation in the September quarter may be higher than expected at the time of the August Statement on Monetary Policy.”

The RBA remains extremely rose coloured about the economy. It says that “Data for the June quarter show that private demand is recovering a little more rapidly than expected, taking over from public demand as the driver of growth.”

And yeah, great. Private demand SHOULD be a bigger driver of growth than the public sector. That finally happening is not a case of hot times in the economy, but more that things are no longer terrible

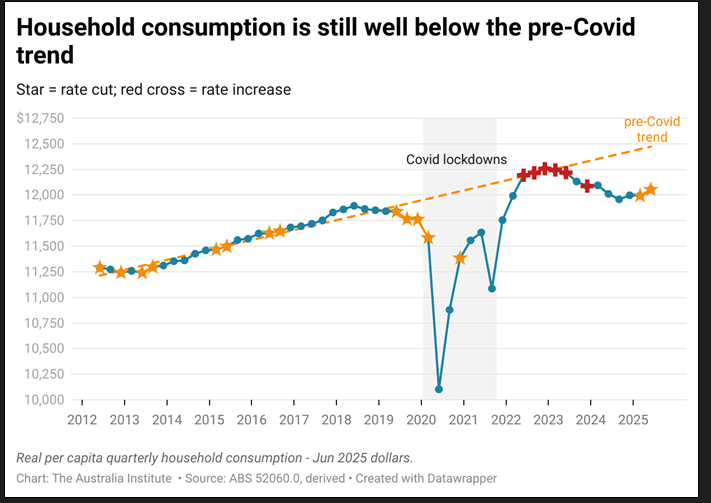

They also noted that “In particular, private consumption is picking up as real household incomes rise and measures of financial conditions ease.” And yeah, the growth is picking (because the RBA is no longer smashing us) but the total is still well below anywhere that you would suggest was strong:

As for the downsides? Pfft The RBA see no problems:

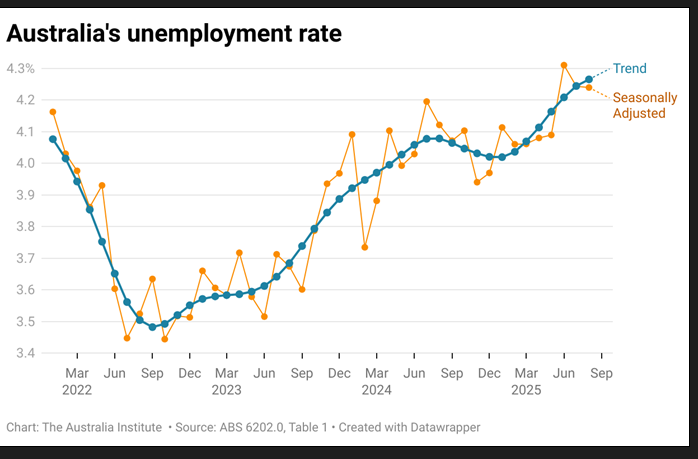

“Growth in employment has slowed by slightly more than expected, but the unemployment rate was unchanged at 4.2 per cent in August.” Slowing employment growth? No biggie. Unemployment steady in August? Yeah ok, but let’s not pretend we don’t know which way it is headed

They also note that “Looking through quarterly volatility, wages growth has eased from its peak, but productivity growth has been weak and growth in unit labour costs remains high.”

First off – measuring productivity is notoriously difficult and never should be looked at in quarterly or even annual growth terms if you are thinking about monetary policy – the point is that wage growth is NOT surging. So what the hell is the RBA worried about?

The comes the uncertainty: “Trade policy developments are nevertheless still expected to have an adverse effect on global economic growth over time. Beyond tariffs, a broader range of geopolitical risks remain a threat to the global economy. This could all weigh on growth in aggregate demand and lead to weaker labour market conditions in the domestic economy.”

The RBA very much is of the school of “let us not help you know because we might need to help you later” school.

In the end “The Board judged that it was appropriate to remain cautious, updating its view of the outlook as the data evolve” – cautious about inflation, but not about employment. But then full employment is only half of the RBA’s mandate, why care about that?

14.41 AEST

The view from Matt Grudnoff

Matt Grudnoff

Senior Economist

In its reasoning on why the RBA has kept interest rates on hold they said

“Uncertainty in the global economy remains elevated. There is a little more clarity on the scope and scale of US tariffs and policy responses in other countries, suggesting that more extreme outcomes are likely to be avoided. Trade policy developments are nevertheless still expected to have an adverse effect on global economic growth over time. Beyond tariffs, a broader range of geopolitical risks remain a threat to the global economy. This could all weigh on growth in aggregate demand and lead to weaker labour market conditions in the domestic economy.”

Translation: Things are uncertain but all the uncertainty points to slower growth.

But slower growth makes the case for a rate cut stronger. Lower interest rates will increase consumer spending and help grow the economy.

Economic growth is only 1.8%, almost half the long run average of 3.3%. Now is the time the RBA should be cutting rates to help the economy.

14.40 AEST

Sigh

The RBA has a habit of really wanting to see the data before it acts. So while it has the monthly data, it doesn’t actually do anything with it until it sees the averaged out quarterly data (the ABS has recently started the monthly data release, but it is still working on tidying it up, so it makes the RBA nervous)

Maintaining price stability and full employment is the priority.

With signs that private demand is recovering, indications that inflation may be persistent in some areas and labour market conditions overall remaining stable, the Board decided that it was appropriate to maintain the cash rate at its current level at this meeting. Financial conditions have eased since the beginning of the year and this seems to be having some impact, but it will take some time to see the full effects of earlier cash rate reductions. The Board judged that it was appropriate to remain cautious, updating its view of the outlook as the data evolve. The Board remains alert to the heightened level of uncertainty about the outlook. It noted that monetary policy is well placed to respond decisively to international developments if they were to have material implications for activity and inflation in Australia.

The Board will be attentive to the data and the evolving assessment of the outlook and risks to guide its decisions. In doing so, it will pay close attention to developments in the global economy and financial markets, trends in domestic demand, and the outlook for inflation and the labour market. The Board is focused on its mandate to deliver price stability and full employment and will do what it considers necessary to achieve that outcome.

14.31 AEST

RBA banks on higher unemployment, more pain

Glenn Connley

Today’s decision by the Reserve Bank of Australia to keep interest rates on hold will force more Australians into unemployment and, ultimately, into poverty.

Greg Jericho, Chief Economist at The Australia Institute, describes the decision as “very cruel”, ensuring more pain for those struggling with high mortgage repayments, and more job losses.

He says all the key economic data supported another interest rate cut, which would have given borrowers much-needed relief after three difficult years.

“The Reserve Bank has once again chosen to be content with rising unemployment,” said Greg Jericho, Chief Economist at The Australia Institute.

“While there have been some signs of improved household spending, the major reason for the increase has been the recent interest rate cuts, rather than an underlying strength in the economy.

“The last recent GDP figures showed the economy still growing at barely half the long-term average, while unemployment has been rising steadily for all of this year.

“The opportunity to lock in unemployment at 4% is fast disappearing due to the Reserve Bank believing there needs to be more people unemployed in order to keep inflation below 3%.

“For those Australians forced to live in poverty on Jobseeker, this is a very cruel decision.”

14.30 AEST

RBA holds interest rates steady at 3.6%

Quell surprise. The RBA has not changed the rate.

14.16 AEST

Liberal Party concerns about more politicians can be easily addressed

Bill Browne

Director of the Democracy & Accountability Program

Former Liberal minister George Brandis is more ambivalent. He argues in the Nine papers this week that: “The argument for increasing the size of the parliament is a respectable one” because of Australia’s growing population but that an increase would favour the Labor Party in the House of Representatives and the Greens in the Senate.

Brandis cites concerns from Liberal–National Senator James McGrath, suggesting these views are held by currently serving Coalition MPs as well.

An increase in the House of Representatives would increase seats everywhere, with no obvious partisan benefit.

And the corresponding increase in the Senate would benefit the Greens less than almost any other party!

This year, I have criticised the Albanese Government for some blatantly self-interested decisions. But there is no reason to believe an increase in the number of politicians would fall into that category. The main beneficiaries of an increase? Voters and Australian democracy.

14.14 AEST

Anika Wells meets with Optus owners

The Optus Triple 0 fall out continues. The communications minister met with Optus owners Singtel about the Triple 0 failure two weeks ago, which had devastating impacts for people calling for help and finding their calls unable to go through.

Wells said the group have promised to restore trust in the system:

I also asked Optus to appoint external accountability to make sure that Australians can take advice not just from Optus themselves but from an independent and external party that the systems in place in Optus will serve Australians when they need the most.

13.52 AEST

And that is it – these last doorstops at the airport (or the hotel lobby before the airport) on these trips tend to be very short because they are just responding to some of the domestic issues of the day – so it’s a whoosh whoosh press conference if you will.

Usually the media and politicians are sick of each other by this point and are just getting some grabs to settle down their newsrooms back home.

13.50 AEST

And on the Trump administration giving the Aukus deal a tick after its ‘review’ (a reminder that Australia remains the only Aukus nation which has not reviewed the deal):

Well, the AUKUS review remains ongoing, but we’ve been participating very constructively with it, and AUKUS has been meeting its milestones. And that is why, in discussions I’ve had with the United Kingdom and with the United States, there has been support for it. We know that AUKUS is in the interests of Australia, the United Kingdom, and the United States. It is about a partnership which is in the interests of all three nations, which will make peace and security in our region so much stronger.

And on Optus’s response to the Triple 0 outrages:

Well, we’re not satisfied with any of Optus’s behaviour. Optus has let down its customers and it’s let down the nation. There will be, of course, ongoing investigation into how exactly this has occurred. Minister [Anika] Wells has been very strong, as is entirely appropriate here, for what is an unacceptable failure of service by Optus to its customers and to the nation.

13.48 AEST

Anthony Albanese press conference

The prime minister is still in the UAE – he is holding a press conference just before he hops on the plane to come home after his 11-day trip to the US and UK (the UAE was a little side stop on the way back to discuss a few things, including bringing a new supermarket competitor to Australia)

Let’s tune in on some of what he is saying:

On the Trump Gaza deal:

Australia has long called for a ceasefire. We’ve called for the hostages to be released and for Hamas to give up its arms. I certainly have welcomed the opportunity to discuss the plans for a ceasefire moving forward over the past week with a range of leaders.

Australia affirms the plan’s commitment to denying Hamas any role in the future governance of Gaza, calls on Hamas to agree to the plan, lay down its arms, and release all remaining hostages. Australia wants to see aid given to the desperate people of Gaza who need this peace plan. We commend the focus which is there in the plan for Palestinian self-determination and statehood, and the Palestinian Authority’s support for the plan, along with so many other nations in the region and countries which have large Muslim populations such as Indonesia and Pakistan. Australia urges all parties to engage seriously with the plan, and to work to bring its vision into reality without delay. Together with our partners, Australia will continue to support efforts to end the war and work towards a just and sustainable two-state solution.

13.44 AEST

Senior economist Matt Grudnoff has written on the ‘fearful and frozen’ RBA ahead of today’s decision:

The RBA has cut interest rates three times this year and each time it has come in the board meeting after the Australian Bureau of Statistics has released its quarterly read on inflation. It seems that each time it cuts rates, it needs to be reassured about where inflation is.

This means that interest rates are being set for where the economy was four months ago and not where it will be in the next year.

Each time the board has got its forecast wrong, it has been because it has misjudged how unemployment impacts inflation.

Recently it has been overly concerned that unemployment is too low. It wrongly believes that businesses face a shortage of workers that will lead to rapidly rising wages, which in turn flow into higher prices and higher inflation.

Despite this, inflation has steadily fallen.

With the ABS not releasing its next quarterly inflation figures until the end of October, we are unlikely to see the RBA act until its November meeting.

The ABS did release monthly inflation figures last week, but these are far less reliable than the quarterly numbers. The bank has consistently said the monthly figures have little impact on its interest rate decisions.

For the 12 months to August, inflation increased to 3 per cent, but at the same time prices in August fell 0.1 per cent. The RBA’s preferred measure, the underlying rate was 2.6 per cent. This is almost exactly in the middle of its inflation target band of 2-3 per cent.

The Reserve’s inability to understand the drivers of inflation spells ongoing problems for Australia. By always looking backwards, it is reducing the effectiveness of monetary policy.

But it also means that unemployment is higher than if it better understood what was happening.

Anthony Albanese has released a statement on the Trump Gaza plan:

Australia welcomes President Trump’s plan to bring peace to Gaza after almost two years of conflict and a devastating loss of civilian life.

Australia has consistently been part of international calls for a ceasefire, return of the hostages, and flow of aid to Gaza.

I welcomed the opportunity to discuss this plan with other leaders over the past week.

Australia affirms the plan’s commitment to denying Hamas any role in the future governance of Gaza, and calls on Hamas to agree to the plan, lay down its arms and release all remaining hostages.

We commend the plan’s focus on Palestinian self-determination and statehood, and the Palestinian Authority taking back effective control of Gaza. President Trump’s plan reflects a clear rejection of annexation and forced displacement of Palestinians.

We acknowledge the diplomatic efforts to include Palestinian, Arab and other key partners’ views in this plan, as demonstrated by the statements of support from the Palestinian Authority.

Australia urges all parties to engage seriously with the plan and to work to bring its vision into reality without delay.

Together with our partners, Australia will continue to support efforts to end the war and work towards a just and sustainable two-state solution.

13.19 AEST

Our mate Donald

Angus Blackman

Podcast Producer

As Trump takes a sledgehammer to American democracy, Australia’s leader snagged a selfie – and a one-on-one meeting in October. How that will go is anyone’s guess.

On this episode of After America, Crikey’s Charlie Lewis joins Dr Emma Shortis to discuss the apparent obsession of Anthony Albanese’s opponents with that bilateral meeting, the transformation of the Republican Party under Trump, and how Australia’s political landscape is being influenced by MAGA.

13.16 AEST

The view from Grogs

Greg Jericho

Chief Economist

There is absolutely no expectation that the RBA will announce a rate cut today at 2:30pm.

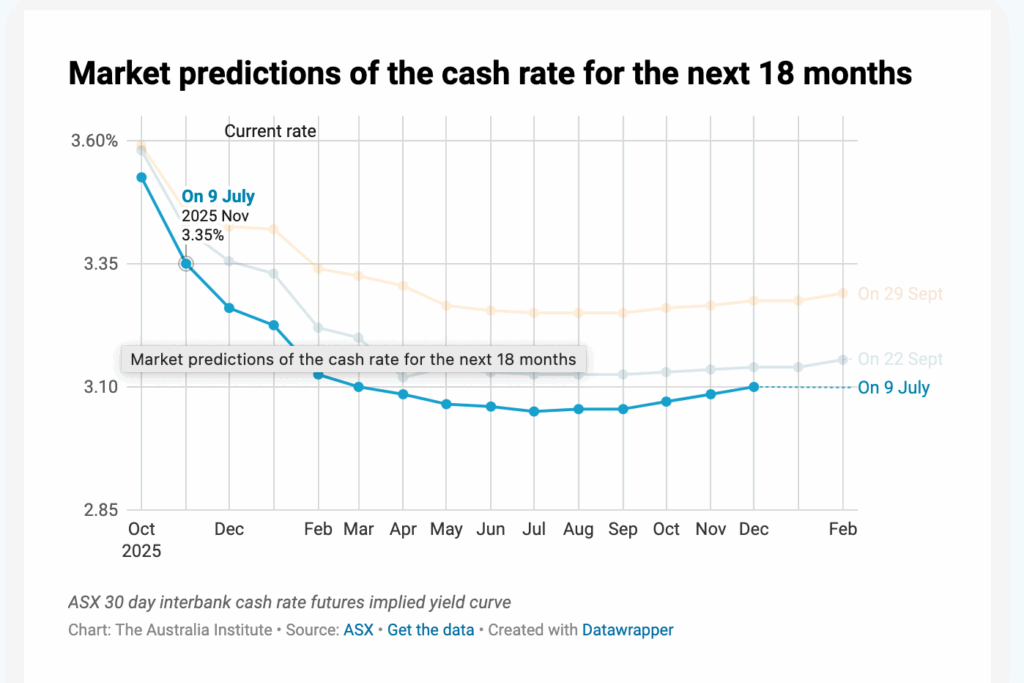

Back in July investors were betting that there would be a rate cut by November and two by March next year. Now the RBA is not expected to cut rates at all until March:

At 2:30pm we will get the reasons from the RBA monetary policy board.

In August, when it did cut rate, the board said “The Board nevertheless remains cautious about the outlook, particularly given the heightened level of uncertainty about both aggregate demand and potential supply” and I suspect uncertainty will again be the order of the day in its statement.

It is worth remembering that while it did cut rates in August, it didn’t in July, when everyone expected they would. Back then the board said “Nevertheless it remains cautious about the outlook, particularly given the heightened level of uncertainty about both aggregate demand and supply.”

So yeah, sometimes uncertainty means we need a cut, sometimes it is the excuse not to cut.

It is worth noting that the most recent GDP figures showed the economy in the first 6 months of this year grew only at an annualised rate of 1.7% – a fair way below the long-term average of between 2.75% and 3% that is needed to stop unemployment from rising.

This year, unemployment has been rising this year, and seems headed to 4.5%, which is pretty sad given in December there was very much the hope of locking in 4% as the ceiling.

But the RBA thinks we need more people out of a job so we all won’t feel confident about bargaining for better wage rises and instead will be content that we have a job.

13.13 AEST

Hello! Welcome to RBA decision day

Good afternoon and hello and missings from the Australia Institute Live crew. We thought we would drop by for a few hours to help guide you through the RBA’s decision on interest rates.

Spoiler: it looks like the RBA board is going to continue to be cowards and not actually move on rates, despite all the indications showing the economy is slowing down. We’ll bring you some of why that is a silly decision, as well as the reaction when the rate decision is made.

Ready? I’m on my third iced matcha, so let’s get into it.

Comments

Start the conversation